The Truth in Savings Act (TISA) is a federal financial regulation law passed in 1991. The act is a part of the Federal Deposit Insurance Corporation Improvement Act of 1991. The law requires financial institutions to disclose to consumers the rates of interest and fees associated with an account.Accordingly, what must a bank provide you upon your request under the Truth in Savings Act?

Under the Truth in Savings Act, banks are required to disclose the annual percentage yield, or APY, and any fees that are associated with the account when you open a savings account or certificate of deposit.

Likewise, what is a Truth in Savings disclosure? The Truth in Savings Act requires the clear and uniform disclosure of rates of interest (annual percentage yield or APY) and the fees that are associated with the account so that the consumer is able to make a meaningful comparison between potential accounts.

Also know, what is the Truth in Savings Act and its importance?

DEFINITION of Truth in Savings Act The act was implemented under Federal Regulation DD. The Truth in Savings Act was designed to help promote competition between depository institutions and make it easier for consumers to compare interest rates, fees, and terms associated with savings institutions' deposit accounts.

Which accounts are covered by Tisa?

TISA covers all consumer accounts which most banks offer.

These include traditional accounts, such as:

- Checking accounts.

- Savings accounts.

- Money Market accounts.

- Certificates of Deposit (CDs)

What does the Truth in Lending Act do?

The Truth in Lending Act (TILA) of 1968 is a United States federal law designed to promote the informed use of consumer credit, by requiring disclosures about its terms and cost to standardize the manner in which costs associated with borrowing are calculated and disclosed.Which of the following created the Truth in Savings Act?

The law requires financial institutions to disclose to consumers the rates of interest and fees associated with an account. The Truth in Savings Act, as part of the Federal Deposit Insurance Corporation Improvement Act of 1991, was signed into law by President George H.W. Bush (R) on December 19, 1991.What is regulation dd?

What Is Regulation DD? Regulation DD is a directive set forth by the Federal Reserve. Regulation DD was enacted to implement the Truth in Savings Act (TISA) that was passed in 1991. This act requires lenders to provide certain uniform information about fees and interest when opening an account for a customer.What is APY rate?

APY stands for annual percentage yield. Banks are required to prominently display this rate for their deposit accounts, like savings accounts and certificates of deposit (CDs). APY gives you the most accurate idea of what your money could earn in a year.What should you know when choosing a financial institution?

The top ten things you should consider when choosing a banking institution are: Security of your funds. Make sure that any bank or credit union is insured by the Federal Deposit Insurance Corporation (for banks) or the National Credit Union Association (for credit unions.)How long must depository institutions retain records under Tisa?

Section 1030.9(c) of Regulation DD requires depository institutions subject to TISA to retain evidence of compliance with the regulation for two years after the date disclosures are required to be made or action is required.When was the Electronic Funds Transfer Act signed into law?

In 1978, the U.S. Congress passed the Electronic Fund Transfer Act—also known as Regulation E—in response to the growth of ATMs and electronic banking, and the Federal Reserve Board (FRB, the Fed) implemented it.How is APY calculated?

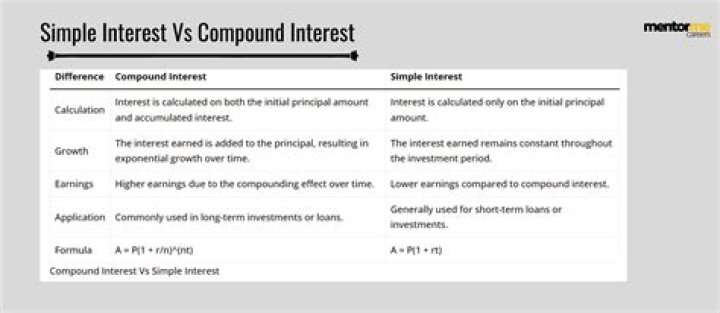

Annual percentage yield (APY) is calculated by using this formula: APY= (1 + r/n )n n – 1. In this formula, “r” is the stated annual interest rate and “n” is the number of compounding periods each year. The more frequent the compounding, the more your money will grow over time.How do I report a bank to the FDIC?

About FDIC To determine which regulator has jurisdiction over a particular banking institution, so you can submit a complaint to the correct agency, you can call the FDIC toll-free at 1-877-ASK-FDIC (1-877-275-3342).What must happen before disclosures can be provided by email or website?

If a consumer who is not present at the institution uses electronic means (for example, an Internet Web site) to apply to open an account or to request a service, the disclosures must be provided before the account is opened or the service is provided.What time account has no required subsequent disclosures?

Subsequent account. When funds are transferred following maturity of a nonrollover time account, institutions need not provide account disclosures unless a new account is established.What is Regulation D in banking?

The federal rule, also known as Reg D, comes from the Federal Reserve Board and puts a limit of six transactions per month on certain transfers and withdrawals from your savings or money market account. » Skip ahead for a comparison of three banks that will help you maximize your savings.What is Regulation E?

Regulation E is a Federal Reserve regulation that outlines rules and procedures for electronic funds transfers (EFTs) and provides guidelines for issuers and sellers of electronic debit cards.What is a MMA investment?

A money market account (MMA) or money market deposit account (MMDA) is a deposit account that pays interest based on current interest rates in the money markets. Money market accounts should not be confused with money market funds, which are mutual funds that invest in money market securities.What does Reg CC stand for?

Regulation CC (“Reg Double C”) A federal banking regulation regarding the availability of funds and collection of checks,Reg CC sets limits for the length of time a financial institution may place a hold on the use of funds after a check has been deposited to an account.What is the purpose of Regulation DD?

Regulation DD (12 CFR 230), which implements the Truth in Savings Act (TISA), became effective in June 1993. The purpose of Regulation DD is to enable consumers to make informed decisions about their accounts at depository institutions through the use of uniform disclosures.Does Regulation D apply to business accounts?

Regulation D covers savings deposit accounts, including conventional savings accounts, high-yield savings accounts, and money market accounts. Under Regulation D, certain types of transactions from savings deposit accounts are limited, meaning you can only make six per statement cycle.